Stop Just Thanking Veterans. Start Funding Them.

Veterans come home with the skills to build great companies yet the financial system treats their service as a liability.

In the summer of 1965, a Yale undergraduate named Fred Smith wrote a term paper about the economy and a logistics company that could deliver packages overnight across the country. His professor gave it a C.

Six years later, after two tours in Vietnam as a U.S. Marine and 200 combat missions, Smith came home with a Silver Star, a Bronze Star, two Purple Hearts, and launched a company out of Memphis, raising $91 million in venture capital.

That company became the most important shipping network in American history: FedEx.

Last week, I was with his daughter, Samantha Smith, investing tens of thousands of dollars in five veterans and military spouse entrepreneurs selected from 1,200 applicants through the FedEx Founders Fund. Samantha and I spoke, and she got choked up talking about her father, who passed this past year and is buried in Arlington National Cemetery. He used to proudly say: “If you can fly a plane, drive a truck, or carry a box - and are a veteran - you have a job at FedEx.” We’re now part of his legacy through this initiative.

Military service and business execution have always shared the same DNA — the discipline, logistical problem-solving skills, and relentless forward movement tend to make for good founders. Smith had all of it. What he also had, crucially, was access to capital.

If Smith were coming home today, the financial system we’ve built might have stopped him before he ever got started.

A recent Milken Institute report, Improving Capital Access for Veteran Entrepreneurs and Military Spouses, puts a number to what many veterans already know. Veteran-owned businesses apply for financing at roughly the same rate as non-veteran businesses — but 60% reported receiving less than they requested, compared to 52% of non-veteran businesses.

Think about what that gap looks like in practice. A veteran who led 12 people under fire comes home, builds a $2 million/year revenue business, walks into a bank, and gets denied a $75,000 working capital loan because two deployments created gaps in his credit history and the underwriting model reads that as financial inconsistency.

The 82nd Airborne Division paratroopers I served with in Iraq never lacked discipline, resilience, or follow-through. What they often lacked when we came home was a financial system that understood what service actually looks like on paper.

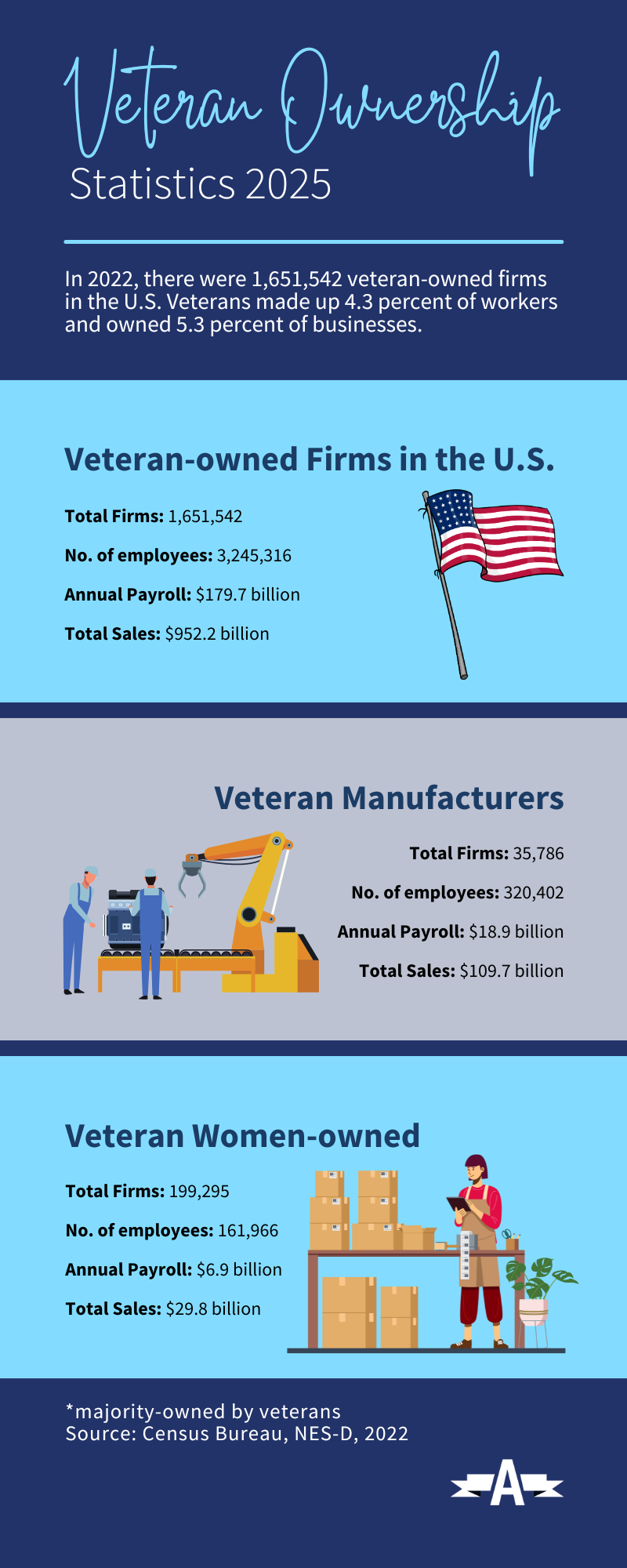

And the scale of what’s at stake here tends to get lost. There are 1.65 million veteran-owned businesses in this country generating $952 billion in annual sales and $180 billion in payroll. Advocating for veteran entrepreneurs is not a sympathetic edge case. Supporting veterans is more than just discounts. It’s a major pillar of the American economy and we are systematically undercapitalizing it. When half the WWII veterans came home and founded iconic brands like Walmart, Nike, and Comcast, they built the American middle class as we know it. But today, less than 5% of my brother and sister veterans from Iraq and Afghanistan have followed the entrepreneur journey. Access to capital is clearly a problem.

At a moment when the country is focused on domestic resilience, industrial strength, and ownership transition, this should be treated as an infrastructure problem.

Here’s how the math works against them. Say a veteran needs $75,000 to hire a first employee or fulfill a contract. That’s not a big loan — it’s a working capital bridge. But for a bank, a $75,000 loan costs almost as much to underwrite as a $750,000 loan, and yields a fraction of the return. So the bank passes and the veteran applies somewhere else. That institution wasn’t designed for small-dollar lending either. Another pass.

The denial isn’t a judgment on the business. It’s a judgment on the loan size.

Then there’s personal credit, which can be even more damaging. Between frequent relocations, deployment gaps and interrupted employment transitions, military life produces exactly the kind of credit profile that underwriting models penalize. Veterans are nearly 3.5 times more likely than non-veterans to cite personal credit history as what’s blocking their access. A 2019 analysis by the Institute for Veterans and Military Families (IVMF) at Syracuse University found 24% of veteran business owners reported being turned down for credit, compared to 18% of non-veterans. Underwriting models don’t distinguish between someone who missed payments and someone who was serving overseas.

And even when the loan comes through, they’re often late and partial. A business owner who needed $75,000 in March to fulfill a contract gets $40,000 in June. The contract window closes. The hire doesn’t happen. The next application goes in with a weaker balance sheet, which means worse terms, which means the cycle repeats.

This is structural friction, and it’s exactly what the Milken Institute is working to reduce alongside a network of partners through its Initiative for Inclusive Entrepreneurship (IIE). The IIE is a national effort to design and implement public-private collaborations that open the flow of capital for entrepreneurs and small business owners who have historically been locked out of financing and investment. Increasingly, the Milken Institute is exploring opportunities to apply its learnings under IIE to reduce structural friction for veterans seeking capital.

It’s not that the infrastructure doesn’t exist. There are SBA programs, Veteran Business Outreach Centers, CDFIs, veteran-focused venture funds, and defense tech investors. If you mapped all the institutions that exist to help veteran entrepreneurs access capital, you’d fill a whiteboard.

What’s missing is a coordinated mechanism that puts capital, authority, and entrepreneurs in the same room with the specific purpose of deploying it. Too many potential veteran entrepreneurs are drowning in the sea of goodwill and lack of focus around access to capital.

Right now, a veteran trying to fund their business experiences a sequence of individual conversations that were never designed to connect. The readiness program that helped her write a business plan doesn’t have a relationship with the lender. The lender’s smallest product is twice what she needs. The venture fund wants high-growth tech; she’s building something else entirely. She goes from door to door, and while each door is technically open, she still can’t get the money.

The gap isn’t a lack of institutions. It’s that nobody is responsible for what happens in the space between them.

All of this can be fixed. The research and capital exist. So do the institutions. What’s been missing is the willingness to put the right people in the same room and refuse to let them leave until something actually moves.

On May 6, at the Milken Institute’s Global Conference, I’ll be moderating a conversation on exactly that — capital access, veteran entrepreneurship, and what closing this gap actually requires. You can watch it live here.

Helping veterans become successful entrepreneurs is among my most important missions as an investor, entrepreneur & at the Wharton Business School - what can you do during National Small Business Week and beyond to be part of the solution?

You are right about everything you wrote.. A lot of effort needs to be invested so that realistically veterans start investing after the mission... But there are many obstacles.. Theory and practice are very different.

It is critical that those who protect us be taken care of. Otherwise, why bother ? Something is seriously wrong in the USA , this is negligent and inconsistent with American values.